Why I am shorting Rheinmetall

~3 minutes to read

Rheinmetall is the darling of German retail investors right now. Everyone’s piling in, thinking this stock can do no wrong because European defense is about to skyrocket, right?

But here’s the cold truth: It’s massively overvalued, and I’m betting it’s headed for a fall. As I write this, Rheinmetall is sitting pretty at €1300. I think it will drop well under €1000 per share. Here's why:

1. Revenue Growth Is Solid, But Valuation Is Ridiculous

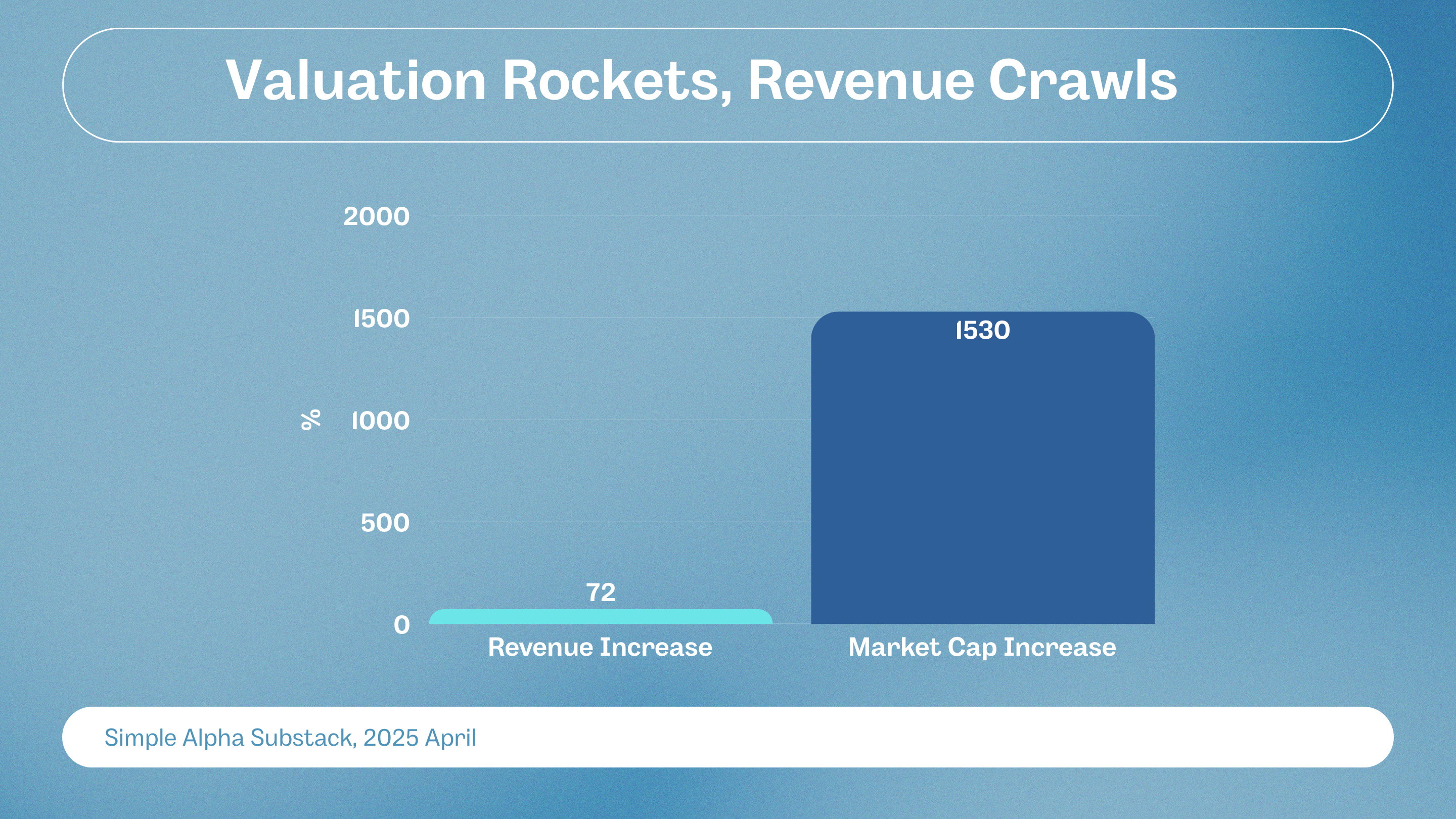

Rheinmetall cranked revenue from €5.66bn in 2021 to €9.75bn in 2024—a 72.4% lift, and EBITDA doubled at 104%. Cool, right? But here’s the kicker: since early 2022, the stock’s rocketed by 1436%—over 15x in three years—while revenue barely doubled. That doesn’t look healthy. But hey, let’s dig deeper.

2. Comparing Apples to... A Really Expensive Orange

Let’s talk comparisons because Rheinmetall doesn’t make sense next to its peers.

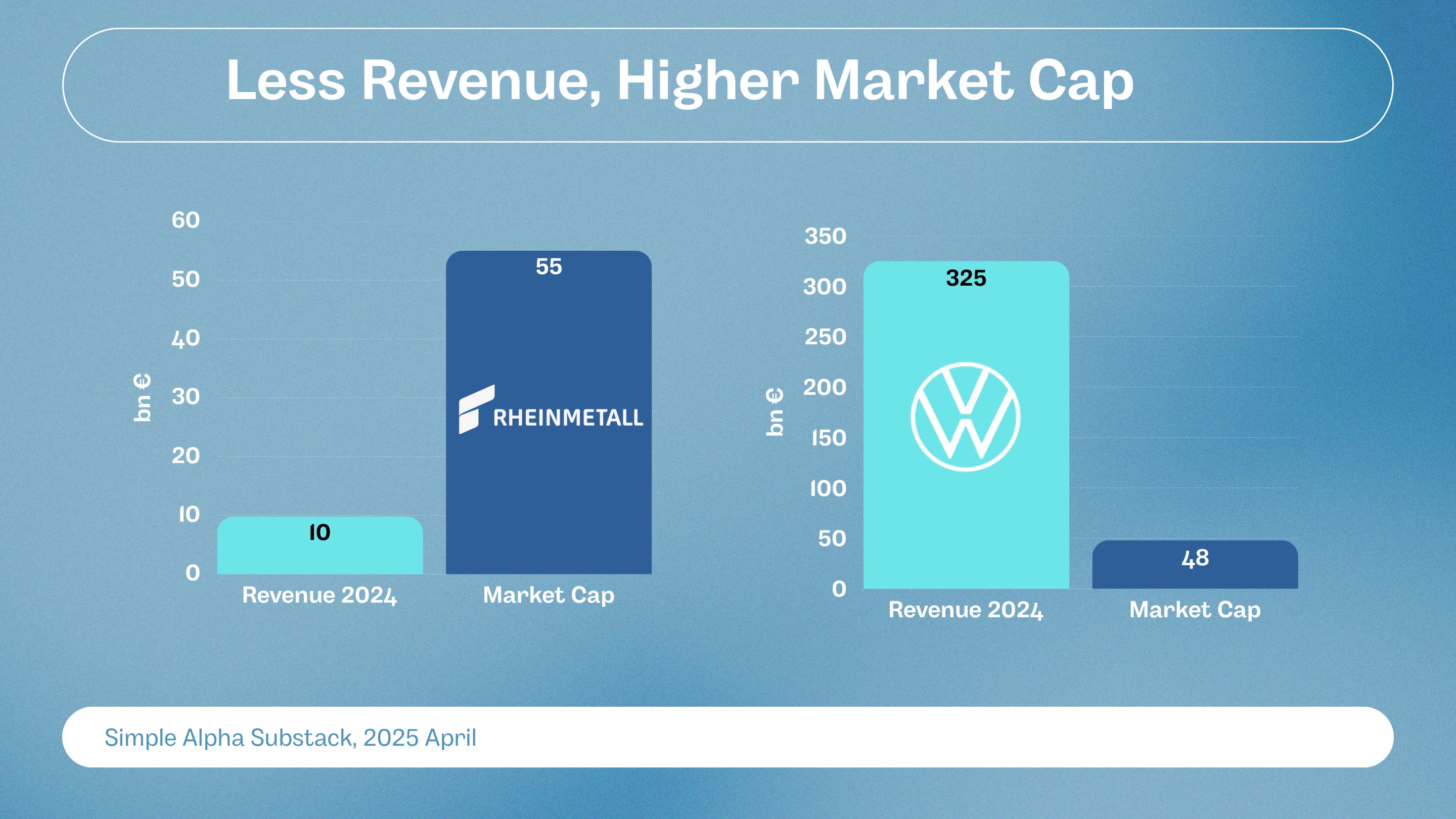

Porsche: 3x the revenue and 90% more net income. But Rheinmetall is valued 2.5x higher.

Volkswagen: 24x the revenue and 7x the net income in Q4 2024. Yet, Rheinmetall’s stock is 10% more expensive than Volkswagen.

What the hell is going on here? A medium size defense company outvaluing one of the largest automakers in the world? That’s suspicious.

Well, you might say: "Defense booms, and German cars suck. Compare it to its real peers." Okay, okay, I hear you.

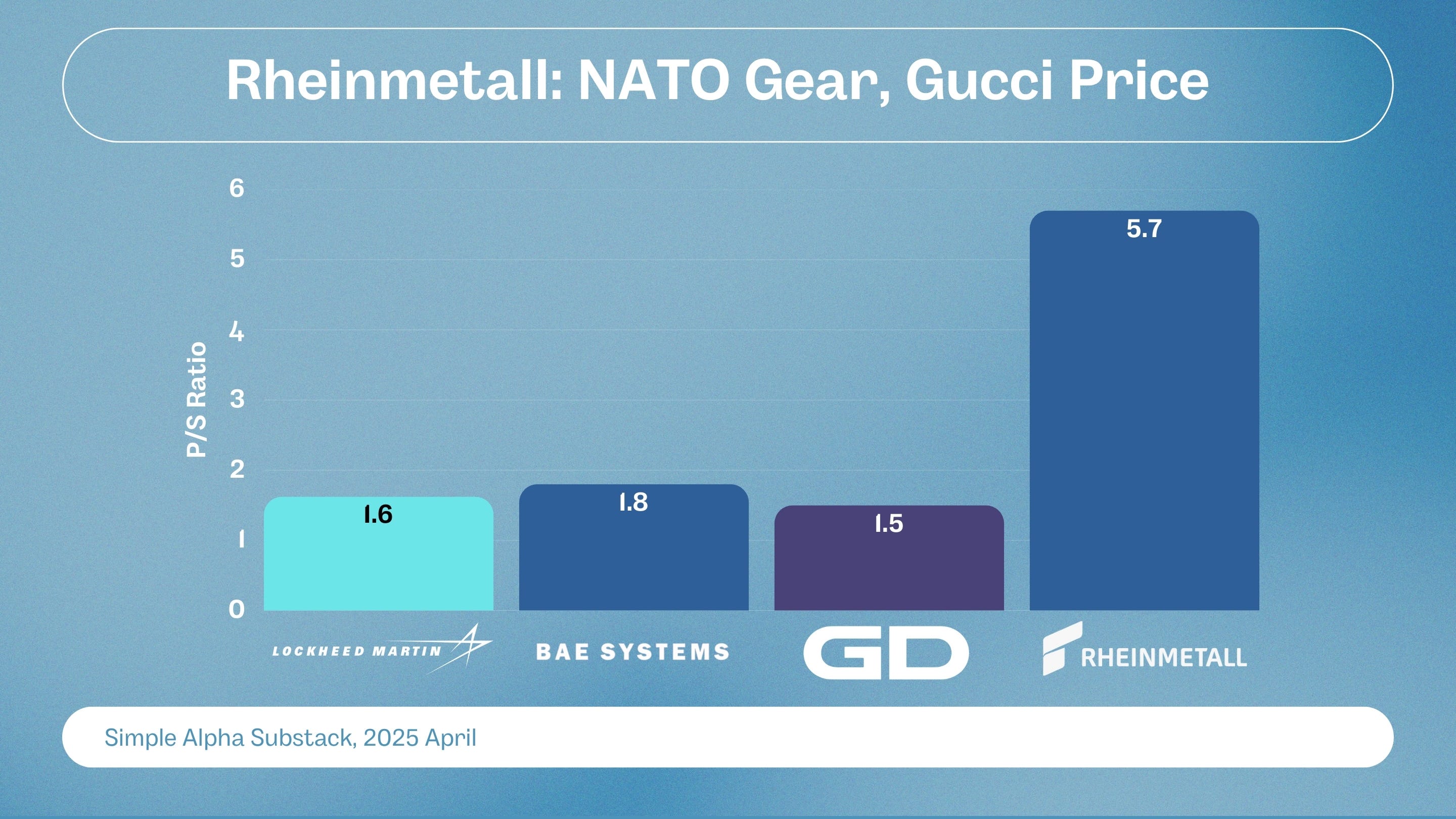

Let’s stack up Rheinmetall against its biggest competitors: Lockheed Martin (US), BAE Systems (UK), and General Dynamics (US). We’ll use the price-to-sales ratio—lower is cheaper.

Yep, Rheinmetall’s sitting on a 3-4x higher sales multiple than its peers. Talk about premium pricing.

3. Boardroom’s Cashing Out

Since March 2025, guess what insiders have been doing? Selling. And not just a little. We’re talking nearly €11m worth of shares. Biggest insider sell-off in over 4 years. The heavy hitters behind this? Experienced board members who’ve been with Rheinmetall for 9+ years. Seems like they’re bailing while the going’s good. Just saying.

4. But David, You Don’t Get It, Rheinmetall Will Outgrow Everything!

Alright, alright, I hear you loud and clear.

Let’s say Rheinmetall somehow manages to double its net income growth rate from 2024—going from 38% to 76%. That would bump net income from €808m to €1.42bn. Now, let’s slap a PE ratio of 25 on that—still higher than its peers. Even with that, Rheinmetall would only be worth €36bn, or €871 per share. That’s 33% lower than where they’re sitting now. And, by the way, a peace deal between Russia and Ukraine? That’d crush Rheinmetall’s value since 10-15% of their revenue is tied to Ukrainian operations. I haven’t even factored that in yet.

Want full transparency? See exactly how my portfolio looks, track my month-to-month performance, and get all the insights—the good, the bad, and the ugly.

Join the paid subscription for €19.95/month. If you don’t make way more than that from my content, I’d be shocked. :)

Love it only question would be why short it now? Don't see the boom dying down in the next weeks.

Not saying I think Rheinmetall is under- or fairly valued. But based on your hypothetical example with 76% net income growth, it should get a lot higher multiple in that case as well than 25. So if it consistently manages to grow that much over a few years, there should be more upside.